European growth capital

Mansion House Is Not Yet a Capital Markets Strategy

The Mansion House Accord is welcome, but a pension-allocation target is not a capital-markets strategy. The test is whether high-quality UK companies can actually access the capital to scale.

The Mansion House Accord is important. But it should not be mistaken for a complete answer to the UK’s capital markets problem.

The headline is attractive: large pension providers committing to put more long-term savings into private markets, with a portion allocated to UK assets. In principle, that should help address one of the UK’s persistent weaknesses. Too much domestic savings capital has become detached from domestic productive investment.

That is a real problem. The UK has good companies, strong universities, deep scientific capability, credible entrepreneurs and a sophisticated financial centre. Yet too many growth companies still find that the capital required to scale is deeper, more patient and more ambitious elsewhere.

Mansion House is an attempt to change that. It deserves credit. But the relevant question is not whether the Accord sounds sensible. It is whether it changes the flow of capital in practice.

So far, the answer appears to be: only partially.

Allocation is not the same as capital formation

There is a significant difference between increasing pension allocation to private markets and repairing the UK capital formation system. Pension capital can flow into infrastructure, property, private equity funds, private credit and larger private assets without materially improving the position of smaller quoted companies, AIM, Aquis, or the next generation of UK growth businesses.

That distinction matters.

The UK does not only need more private markets exposure. It needs better routes for companies to move from early-stage capital to scale-up finance, from private ownership to public markets, and from domestic promise to global competitiveness. That requires more than a pension allocation target. It requires liquidity, research coverage, institutional appetite, governance quality, sensible regulation and a credible equity culture.

What the evidence shows

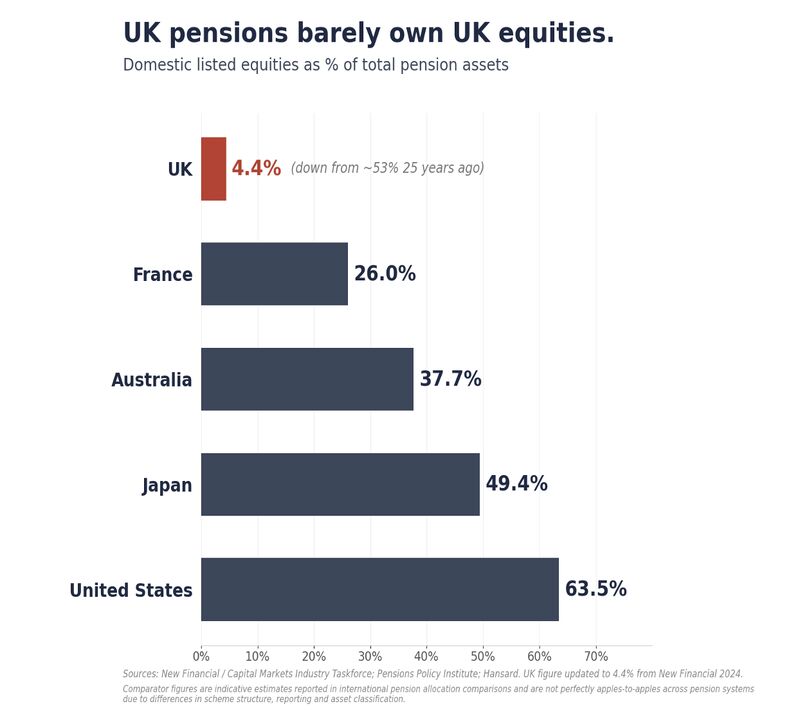

The source material behind the post makes the point clearly. New Financial has argued that the problem is upstream demand for UK equities, not simply the listing regime. The UK pension system has moved dramatically away from equities and away from the domestic market over the past generation. The exact figure changes by source and year, but the direction is unmistakable: UK pensions once had very large exposure to UK listed equities; today that exposure is in single digits.

The Quoted Companies Alliance makes the practical objection. One year on, the Accord has not yet translated into visible capital flows for many smaller public companies. That is not a minor implementation detail. If the capital goes mainly into large private funds and infrastructure assets, the Accord may still be useful, but it will not have solved the public-market part of the problem.

The fiduciary constraint cuts both ways

There is also a fiduciary constraint that should not be dismissed. Pension providers are not national development banks. Their first obligation is to savers. Any allocation to UK assets must stand up on risk, return, diversification, liquidity, cost and governance. “Backing Britain” may be good politics, but it is not by itself an investment case.

At the same time, fiduciary duty should not become an excuse for institutional inertia. A serious pension system should be capable of allocating a sensible portion of long-term capital to productive assets. Other countries have built stronger links between domestic savings and domestic enterprise. The UK should be able to do the same.

The challenge is execution

For policymakers, the task is to make UK assets more investable, not simply to pressure institutions to buy them. That means improving the pipeline of credible opportunities, reducing unnecessary friction, supporting market depth, and making it easier for companies to stay, scale and list in the UK.

For companies, the message is equally clear. Boards should not assume Mansion House will solve their capital problem. They need to make themselves investable. That means sharper equity stories, more disciplined capital allocation, better investor communication, realistic milestones, and governance that earns long-term institutional confidence.

Capital does not flow just because it is encouraged. It flows when opportunity, trust and return come together.

Mansion House may become a useful catalyst. But if the capital primarily flows into large private funds and infrastructure assets while smaller UK quoted companies continue to struggle for attention, then it will not have solved the core problem.

The test is not the size of the pledge. The test is whether more high-quality UK companies can access the capital they need to scale, and whether UK savers are properly rewarded for providing it.

Sources

- Unlocking the capital in capital markets — New Financial / Capital Markets Industry Taskforce.

- The Mansion House Accord: Time for Action One Year On — Quoted Companies Alliance.

- Pension Schemes Act 2026: a guide to the key provisions — Norton Rose Fulbright.

Distribution list

Be told when a new essay is published

Join the distribution list for occasional notes on governance, boards, AI, healthcare and growth capital. No marketing — just new essays.